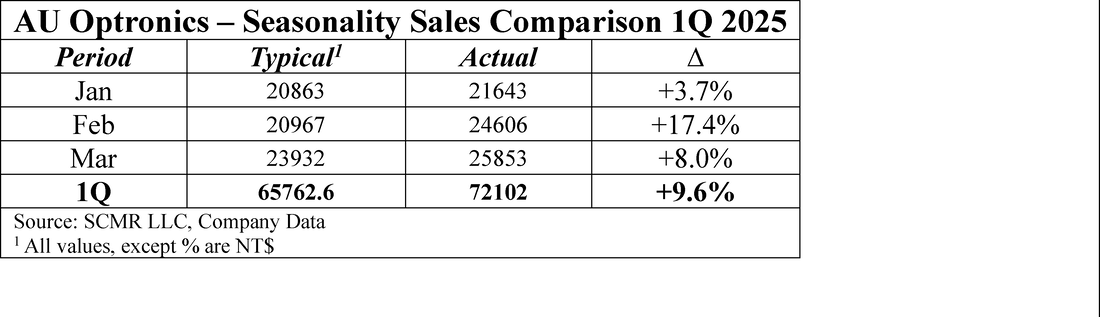

April in Taiwan

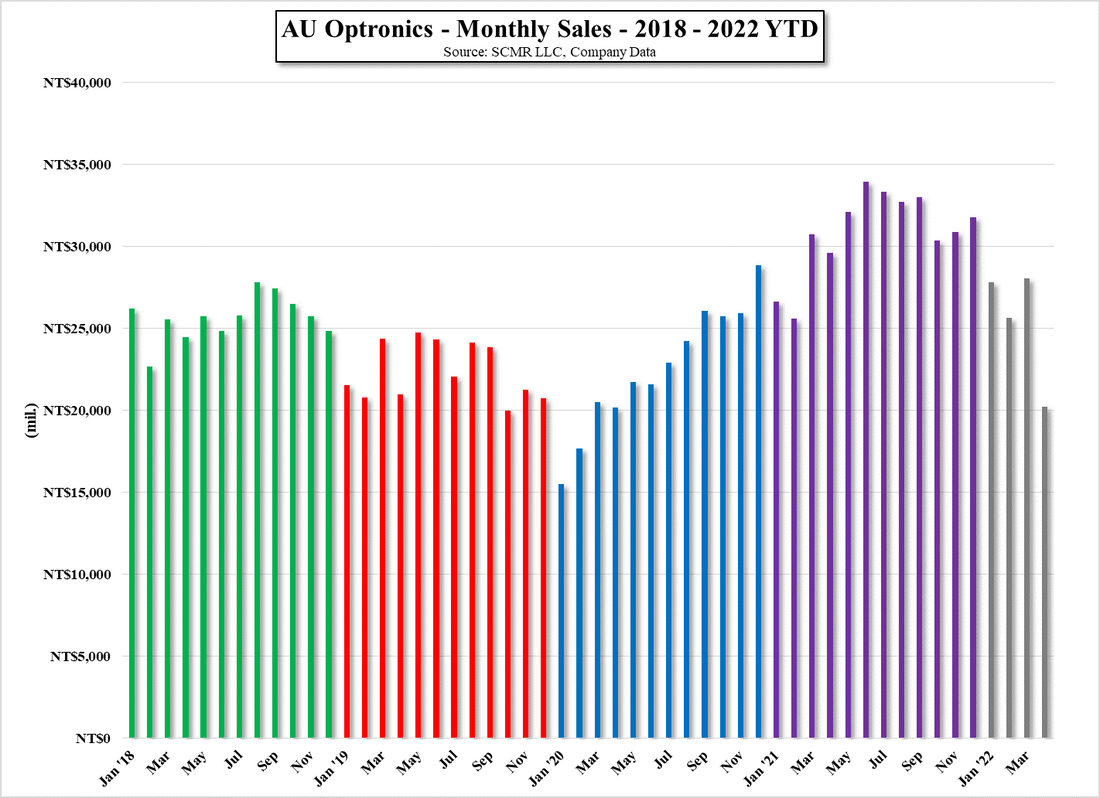

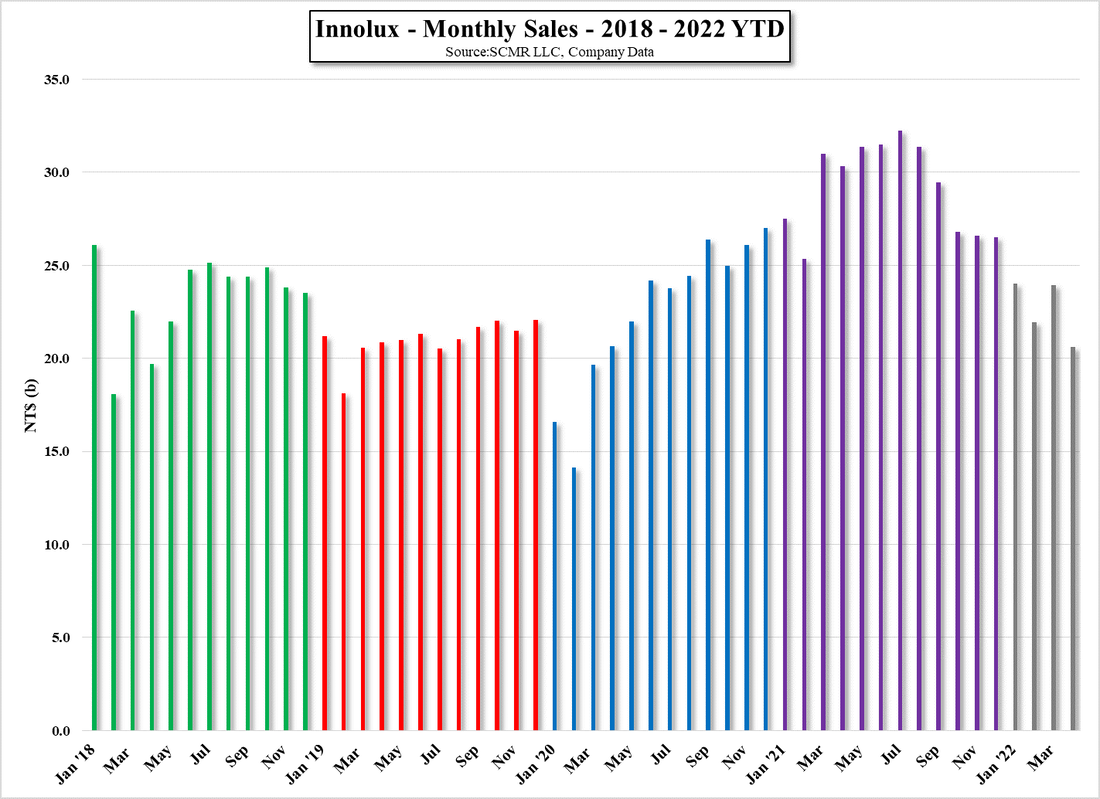

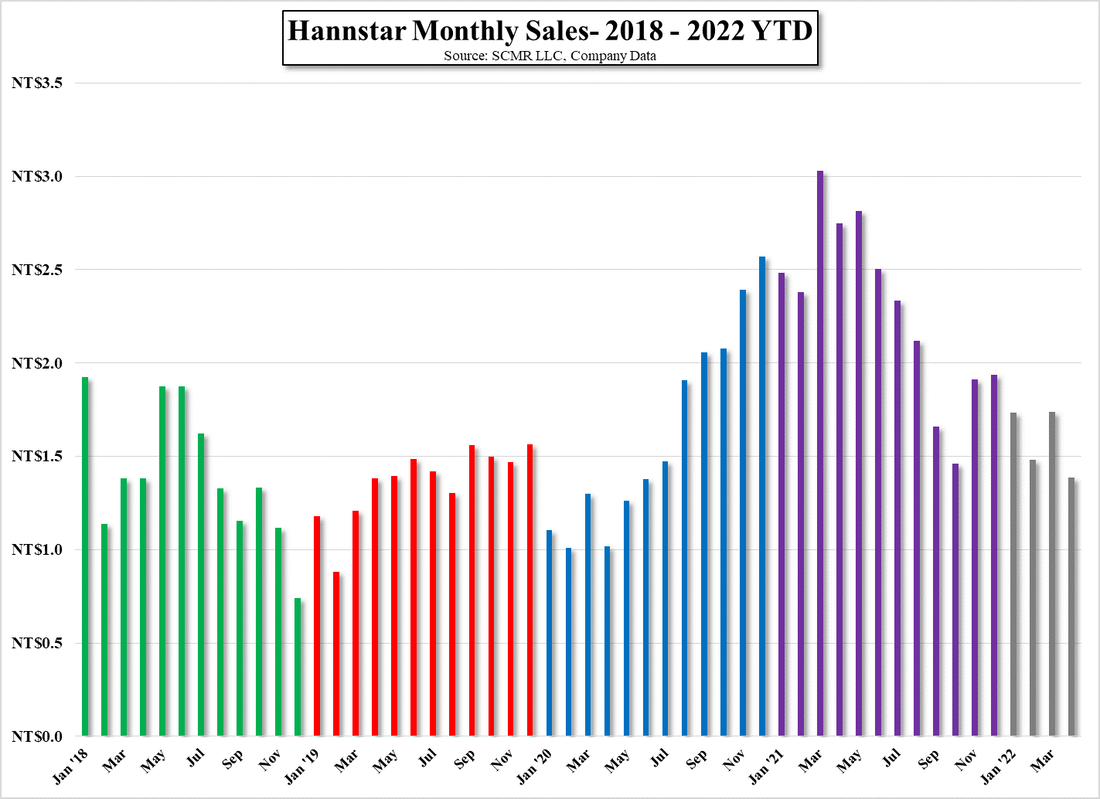

The three panel producers in Taiwan, given the fact that they are required to report monthly sales, tend to be a precursor to general display industry trends, and as such we track sales data for all three. On a general basis AU Optronics (2409.TT) and Innolux (3481.TT) are oriented toward large panel production while Hannstar (6116.TT) is oriented toward small panel production, although all three do both. In April the general trend was for relatively flat sales m/m, although AUO saw m/m sales decline by 10.5% after a strong March.

While each of the three producers have their own sales patterns, the general trend last year was for a weak 1Q and progressive improvement through September. This will make y/y comparisons more difficult going forward this year, which have already turned negative for both large panel producers. As we have noted, there has been some non-linearity this year as CE brands pull in orders to move product into the US to avoid potential tariffs, which we expect will continue until the next ‘tariff deadline’ in early July. Inventory levels in many CE products remain high for the same reason, which could affect production later in the year if there is no incremental demand as the holiday season unfolds in September.

While each of the three producers have their own sales patterns, the general trend last year was for a weak 1Q and progressive improvement through September. This will make y/y comparisons more difficult going forward this year, which have already turned negative for both large panel producers. As we have noted, there has been some non-linearity this year as CE brands pull in orders to move product into the US to avoid potential tariffs, which we expect will continue until the next ‘tariff deadline’ in early July. Inventory levels in many CE products remain high for the same reason, which could affect production later in the year if there is no incremental demand as the holiday season unfolds in September.

Figure 1 - AU Optronics - Monthly Sales - 2018 - 2025 YTD - Source: SCMR LLC, Company Data

Figure 2 - Innolux - Monthly Sales - 2018 - 2025 YTD - Source: SCMR LLC, Company Data

Figure 3 - Hannstar Monthly Sales - 2018 - 2025 YTD - Source: SCMR LLC, Company Data

RSS Feed

RSS Feed